Stay informed with the latest market update. Discover insights into economic trends, investment performance, and the outlook for Canadian and global markets.

What to do when stock market values are down

April 07, 2026

By Sun Life staff

Market values usually go up and down. But what can you do when these values drop a lot? Consider staying invested. Here’s why.

When the stock markets drop drastically, it's natural to want to do something to reduce the volatility. Perhaps you want to sell your investments or make changes to your portfolio. But if you already have a diversified portfolio, that may not be the best thing to do right now.

If you have a diversified portfolio and your financial objectives haven't changed, then the best course of action is to stay invested in the markets.

Why stay invested, even in a volatile market?

Because historically the markets have bounced back and recovered.

"Market declines are uncomfortable, but they are not unusual,” says Christine Tan, Assistant Vice-President, Portfolio Management, Sun Life Global Investments. “As a long‑term investor, the most important discipline is separating short‑term market noise from long‑term financial goals. History consistently shows that patient investors who stay diversified and remain invested are far better positioned to benefit when markets recover.”

Many different events have sparked volatility in the past. Look to history as a guide. Think of Black Monday in 1987, the Tech Meltdown of 2000, or the early days of the COVID-19 pandemic. In all these cases, you’ll see a cycle.

Bottom line: It's natural to feel uneasy when markets are volatile and the news is unsettling. But staying the course and maintaining a long-term perspective can help you navigate disruptions and keep your financial goals on track.

What happens if you sell when the markets are down?

First, you'll turn a paper loss into a real loss. Then, once you're out of the market, you'll have to decide when to get back into the market.

So, what happens when markets recover unexpectedly? You have to be in the market to get the gains that are there. And if you're out of the market, you can suffer significant financial losses over a long period of time.

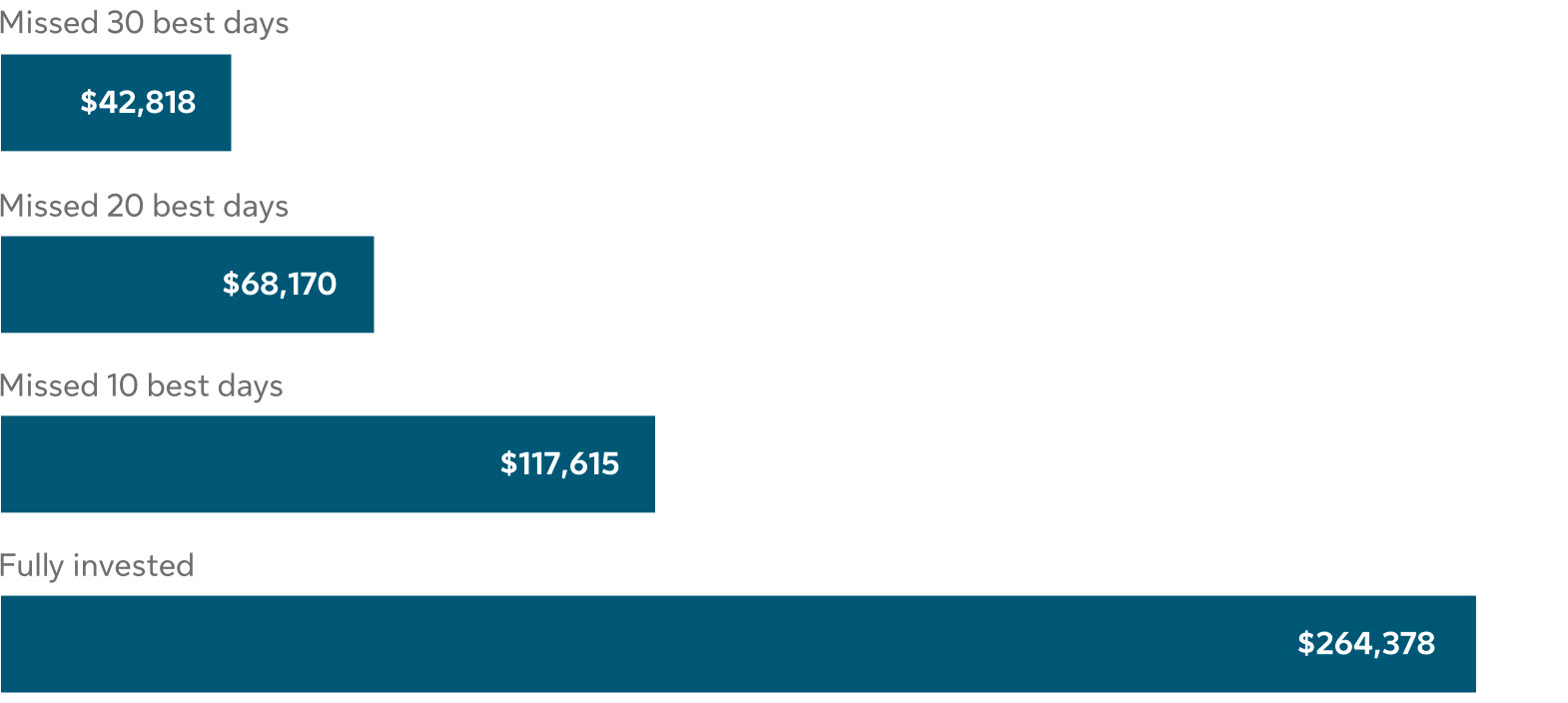

Let's look at an example of a $10,000 investment on January 1, 2005, to December 31, 2025.

For illustrative purposes only. Returns have been rounded to the nearest whole number for simplicity. Past performance is no guarantee of future results. It is not possible to invest in an index. Actual returns would be different due to fees and expenses associated with investing which are not applicable to an index.

Missing just the 10 best days, over 20 years, means a return of $146,763 less than if you just left your money invested. In a worst-case scenario, missing the best 30 days means you’d end up losing a whopping $221,560 on your initial investment!

“Market sell‑offs may even work in favour of disciplined investors,”says Tan. “When markets are down, regular contributions or rebalancing into what has underperformed naturally buys more at lower prices. Over time, that steady approach can enhance long‑term outcomes as markets recover.”

For example, let’s say:

- You contribute the same amount each month to an RRSP that holds mutual funds.

- This month market values are down, compared to the previous month.

- Your contribution this month therefore buys more units in the lower-valued mutual funds than it did the month before.

- Later, if market values rise, you’ll benefit from the recovery, as prices for the units you bought rise.

How can you keep your financial goals on track?

If you want to keep your finances on track, start by asking yourself these three questions:

- Have your financial goals changed?

- Do you have a diversified portfolio?

- How comfortable are you with risk?

You may be better off staying the course and sticking to your original plan if:

- Your goals haven't changed, and

- You have a diversified portfolio.

Remember, history tells us that markets grow over the long term.

“Volatility is not a flaw, but a feature in financial markets that are constantly pricing in new information, whether it’s earnings, economic data or geopolitics,” says Tan. “A well‑constructed, diversified portfolio is designed to weather volatility. Staying focused on your plan, rather than reacting emotionally to headlines, is one of the most important investment decisions.”

5 ways an advisor can help

Are you worried about volatility risk or inflation risk? Or maybe you're concerned that your portfolio lacks diversification? In such cases, talking to a professional may help.

An advisor can help you:

- Make well-informed decisions.

- Understand your risk tolerance.

- Make a plan and build an investment portfolio that meets your long-term goals.

- Feel assured in times of uncertainty, knowing you've taken steps to prepare.

- Avoid making in-the-moment decisions about your savings.

Definition of terms:

Market volatility refers to dramatic swings or ups and downs in the markets.

A diversified portfolio includes various assets like stocks, fixed income, and commodities. These assets may react differently to the same economic event. The value of one may rise while the value of another may fall. This lowers your overall risk because no matter what happens in the market, some assets will still have gains.

This article is for information and illustrative purposes only. It's not intended to provide specific financial, tax, insurance, investment, legal or accounting advice. It does not constitute a specific offer to buy and/or sell securities. We've compiled information in this article and webinar from sources believed to be reliable, but no representation or warranty, express or implied, is made with respect to its timeliness or accuracy.