Diversification: What is it and how can it help reduce your investment risk?

There’s no predicting how well your investments will perform. Will they take a hit during tough economic times? Will they give you steady returns? In the face of market uncertainty, the best investment strategy is to diversify your portfolio. Here’s how diversification can help.

Diversification is a strategy that spreads your risk as an investor over different types of investments. The aim is to balance both the overall risk and your potential returns.

By diversifying, you also help protect your savings from the market’s ups and downs in values. This happens because different types of investments, such as stocks and bonds, often move in different directions. If they do move in the same direction, some investments don’t necessarily move as quickly or as far as other investments.

Here’s what you need to know about diversification – and how it can help you as an investor.

Does diversification help to reduce risk?

If you hold just one investment, you could put yourself at risk. Why? If your investment performs poorly, you could lose your hard-earned money.

To boost your portfolio’s resilience, diversification can help lower the downside pain from a market downturn. It’s unlikely all your investments will perform poorly at the same time. Good returns on some of your investments can balance out the losses on the others, leading to a potentially better experience and more peace of mind.

How can you diversify your investment portfolio?

You can diversify your portfolio by:

- Choosing different investment types (for example, stocks and bonds)

- Varying the level of risk within investment types (for example, low, medium and high)

- Including investments from different regions of the world (for example, Canadian, U.S., European, Asian, emerging markets, etc.) But be aware of currency risk, also known as foreign exchange (FX) risk, which is the possibility of financial loss due to exchange rates.

- Having multiple company sizes in your equity portfolio (large market capitalization, mid-capitalization and small-capitalization)

- Holding investment funds that employ different investment management styles (for example, active, passive, growth, value, etc.)

- Investing in different sectors (for example, financials, technology or health care)

Asset allocation can be an effective way to help manage risk in your investment portfolio.

Simply put, it’s a strategy that involves selecting a mix of investments appropriate to your risk tolerance, time horizon, and financial goals.

What are the most common types of investment assets?

The most common types of investment assets, or asset classes, are:

- cash equivalents,

- fixed income securities, such as bonds or bond funds, and

- equity securities, such as stocks or equity funds.

Each asset class is expected to have different levels of risk and return characteristics. So each will behave differently over time. For example, stocks are typically considered riskier than bonds, but they also offer the potential for higher returns over the long term.

There’s no predicting how well your investments will perform or how steady your returns will be. That’s why it’s important to diversify your portfolio.

What are your asset allocation options by age as an investor?

Are you a young investor saving for retirement? Then you may have plenty of time before you're likely to withdraw the funds. You may consider allocating more of your portfolio to equities. One option would be a split of 70% equities to 30% fixed income.

Are you getting closer to retirement? Then you may want the comfort of a more income-oriented portfolio, with say, maybe only 40% equities and 60% fixed income, even if it means giving up some of the potential for higher growth in exchange for lower, steadier returns.

Diversifying your portfolio over time by increasing the fixed income allocation and decreasing the equity allocation may keep your portfolio stable as you approach goals, such as retirement.

Did you know you can further diversify your portfolio by selecting a mix of securities within each asset class? For example, there are different types of securities according to locations, industry branches, or investment styles.

Because investments within various asset classes may behave differently, it’s a good idea to review and rebalance your portfolio regularly. That will help ensure it holds the right asset mixed, based on your current values, tolerance for risk, time horizon, and financial situation.

Find more tips and tools on sunlife.ca.

What are some of the different types of investments based on their level of risk?

Different investment types each have their own purpose. They have varying levels of risk and potential returns. Let’s break down the types of investments based on their level of risk:

Lower-risk investments

Cash equivalents, such as money market funds, provide low risk returns. They generally include investments such as guaranteed funds and short-term deposits that pay you interest. While the risk is low, many cash equivalents also have low rates of return.

Medium-risk investments

Fixed-income investments, such as bonds, are generally higher risk than cash equivalents. But they offer potentially higher returns. When you invest in bond funds, you lend money to the company or government issuing the bond. They repay the amount of the loan plus interest over a specified period. Bond fund values go down when interest rates go up, and vice-versa.

Higher-risk investments

This includes equity funds which are made up of stocks. These are higher risk than cash equivalents or fixed-income investments. But with higher risk comes a higher potential for long-term growth. Equity funds give you an ownership interest in the issuing companies. If there’s an increase in the companies’ values, you may see investment gains.

How does investment risk vary by age?

Your age tends to dictate how much risk you're willing to take on in your investments.

Early in your career

With retirement decades away, you have time on your side. You can increase your portfolio’s long-term investment risk and set yourself up for higher potential returns.

Mid-career

Retirement is still years away, so you still have lots of time. You’ll want a moderate increase in the long-term investment portion of your portfolio.

Close to retirement

As you near retirement, now's the time to ensure that your portfolio reflects your retirement income goals. This is the time to reduce your portfolio’s investment risk as you approach the years where you will need to be withdrawing from your portfolio.

How can you diversify your investments?

Diversifying within an investment type can make your portfolio more resilient to stock market ups and downs. Since investments react differently to the same event or crisis, returns will be different from one investment to the next. Losses in one area may be offset by gains in another. There are two main ways you can diversify your investments.

1. Explore new regions

Diversifying by region means investing not only in Canadian funds, but also in foreign funds. This strategy increases your chances of growth while managing risk. You benefit from the strength of different markets, while reducing the risks of having all your investments tied to just one region. There are many excellent companies outside of Canada and the United States to invest in; for example, Germany for car companies or pharmaceuticals.

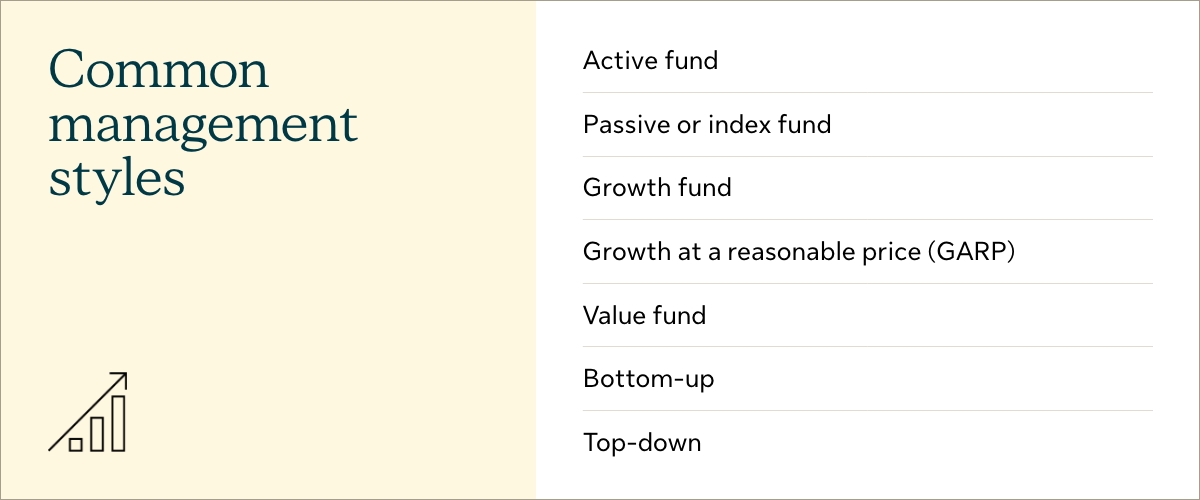

2. Consider allocating to different management styles

Managers apply varying management styles when choosing investments for their funds. Different styles perform well in different economic cycles and environments. Common management styles include:

- Active. Fund managers choose funds they expect will have the best potential returns.

- Index or passive. Managers try to match the returns of an index, such as the S&P/TSX Composite index. They do this by selecting stocks from the benchmark index.

- Growth. Managers invest in companies experiencing a rapid growth in profits.

- Growth at a reasonable price (GARP). Managers look for stocks of growth companies they can buy for a reasonable price.

- Value. Managers search out companies they believe are undervalued by the market.

- Bottom-up approach. Managers focus first on the fundamentals of a company before looking “up” at other factors, such as the economy.

- Top-down approach. Managers examine an industry’s broad economic outlook. Then they look “down” to select stocks from that industry.

Need help diversifying your investment portfolio?

When it comes to investing, it’s important to keep sight of your long-term goals. Diversification is one way to achieve them.

Speak with an advisor about what level of risk is right for you, and how to diversify your portfolio.

They can help you:

- understand what your risk tolerance is, and

- make a plan and build an investment portfolio that meets your goals.

This article is meant to provide general information only. Sun Life Assurance Company of Canada does not provide legal, accounting, taxation, or other professional advice. Please seek advice from a qualified professional, including a thorough examination of your specific legal, accounting and tax situation.