What is term life insurance?

Simply put, all types of life insurance can help provide your loved ones with financial security when you die. One common type of life insurance is called term life insurance.

How does term life insurance work?

Term coverage provides protection for a fixed payment amount, for a given number of years. This could be 10, 15, or 20 or more years. You can choose the amount of time you need.

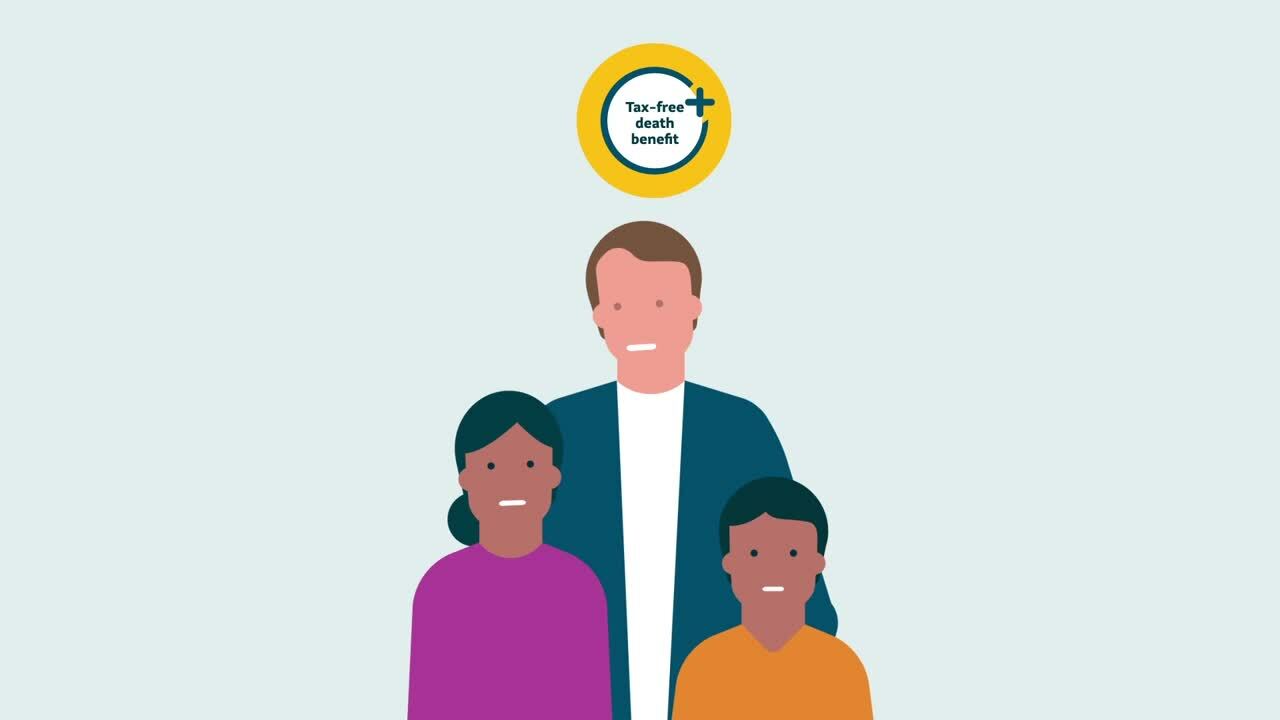

What happens if you die during this set time period? Then your beneficiaries – the people or person you want to leave money behind to – will get a tax-free death benefit.

The death benefit refers to the amount of money your beneficiary gets when you die. The exact amount they get depends on how much coverage you buy.

Your beneficiaries can then use the money from that benefit for any reason. For example, they can use it to pay:

- Debts,

- the mortgage or rent,

- child-care costs,

- tuition costs,

- funeral costs,

- living expenses,

- and more.

Why choose term life insurance?

Because of its affordability and flexibility, term life insurance can be a good solution to help you manage risk, while providing for your dependents.

But its true value lies in the peace of mind it can offer. The assurance your loved ones can be financially supported at a time when they need it most.

For more tips and tools, visit sunlife.ca.