Women co-power Canada’s economy. Learn how Sun Life is committed to empowering women to make positive wealth and health decisions.

New Sun Life research: 38% of surveyed Canadian women reshape financial plans due to life transitions 2025

July 09, 2026

By Sun Life staff

A Sun Life survey of 653 Canadian women finds major life transitions like perimenopause and caregiving responsibilities are interrupting careers and reshaping financial futures. Yet traditional planning models may not be built to handle them.

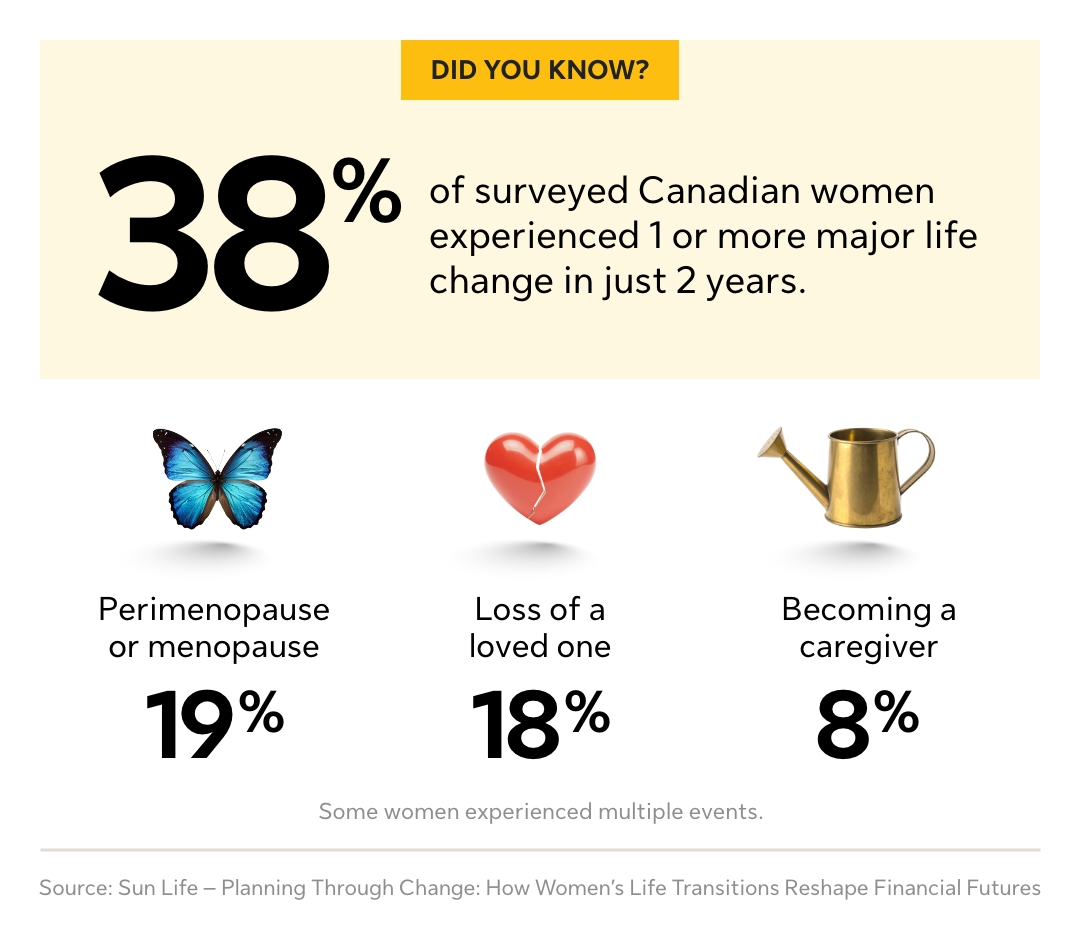

In January 2025, Sun Life partnered with Ipsos to survey 653 Canadian women about how life transitions affect their financial security. The findings reveal a critical mismatch: 38% of Canadian women experienced major life disruptions in the past two years including perimenopause/menopause (19%), loss of a loved one (18%), or becoming a caregiver to a family member/aging parent (13%). Yet most traditional planning models seem to still assume stable incomes and uninterrupted careers.

The disconnect appears consistently across generations and income levels, with younger women bearing the heaviest psychological burden.

Key research findings

Of the 653 women surveyed:

- 40% are more likely to be ‘sandwich caregivers’ supporting both children and aging parents

- Canadian data reinforces this reality: 41% of women caregivers experience financial hardship compared to 28% of male caregivers.1

- Those with high financial confidence accumulate 64% more in savings relative to income demonstrating that confidence drives outcomes 5x more powerfully than literacy alone (12% improvement).

Download the full report: Planning Through Change: How Women’s Life Transitions Reshape Financial Futures

6 life transitions that disrupt women’s financial plans

Of the women surveyed, six life transition points emerge as the most common factors that reshape women’s financial futures:

- Entering the workforce: when foundational money decisions are made

- Maternity/parental leave and caregiving: when income gets interrupted during peak earning years

- Career shifts and relocations: when clarity is needed around cash flow, benefits and long-term security

- Separation, divorce, or loss of partner: when financial independence must be rebuilt under stress

- Health events and aging: where planning must account for rising care costs

- Retirement planning: managing longer lifespans with potentially interrupted savings

3 systemic challenges reshaping women’s financial security

The survey results identifies three challenges impacting the greatest number of women across all demographics and life stages:

Perimenopause/menopause most reported life event: 19% of surveyed women face career and savings disruption

With 19% of women experiencing perimenopause or menopause in just the last two years, it’s the single most reported life transition. Yet most traditional planning models treat this life event as an afterthought.

When health symptoms lead to reduced hours or early retirement, the compounding financial impact can include lost income, missed retirement contributions, reduced pension benefits and eliminated growth potential during peak earning years.

“Because you are a woman, you will experience things that men won’t – like disruptions related to parental leave”, notes Craig Macdonald, Program Director of One Sun Financial Planning at Sun Life Canada. “That can be disruptive to your career, to other aspirations, or even your retirement timeline.”

Women caregivers are more likely to experience financial hardship

40% of the surveyed women were more likely than men to be ‘sandwich caregivers’ who simultaneously care for children and aging parents. Two-thirds report employment impacts, and the financial toll is stark: 41% of women caregivers experience financial hardship versus just 28% of men.

“When women are in a chronic state of caregiving, their personal money management often falls to the wayside,” explains Chantel Chapman, Financial Educator and Co-Founder of the Trauma of Money Institute. “We call it a bandwidth tax – you’re taking care of everyone else, and your own financial needs get pushed back.”

Most surprising finding: financial confidence drives 5x more savings growth than literacy

The survey’s most surprising finding, reinforced by Sun Life’s separate report, Member Mindset and Motivations, indicates that financial confidence can drive outcomes more than knowledge alone. Women with high confidence accumulate 64% more in savings, while those with high literacy but low confidence achieve only 12% improvement.

Yet 20% identify low confidence as a barrier versus only 15% citing low knowledge – suggesting a critical gap between how financial education and advice are typically designed and delivered.

Building financial resilience through career interruptions

Unlike traditional models that often assume steady income and uninterrupted careers, resilient planning anticipates disruption as part of real life, not as an exception.

Financial planning recommendations for unpredictable life events

The full report suggests a few recommendations for women facing life’s inevitable transitions:

- Scenario planning for “what-if” events: modeling income interruptions, family changes, and layered disruptions before they occur

- Stress testing against financial shocks: determining whether your savings and income strategies can withstand market downturns, inflation spikes, and increased longevity

- Protection through insurance and emergency savings: ideally established before the emergency ($5K - $7K recommended), not during it

- Regular checkpoints: treating financial planning as an ongoing process that adapts as life evolves, not a one-time document

“Planning needs to be modular, not monolithic – able to absorb life’s unexpected turns without derailing long-term goals”, says Macdonald.

Women with advisors 2x more prepared for retirement (43% vs. 20%)

The survey results indicate that women with a wealth advisor are twice as likely to feel prepared for retirement (43% vs. 20%) compared to those planning alone. Yet not all advisory relationships are created equal.

The advisors who have the potential to make the greatest impact go beyond income and assets. They create space for goals, responsibilities, concerns, and life transitions. They combine technical expertise with emotional intelligence, recognizing that money decisions during divorce, health events, or caregiving aren’t purely rational calculations.

The report identifies four ways advisors can help clients build lasting financial resilience:

- Embedding emotional check-ins into planning conversation

- Using the ‘small win’ approach that rebuilds confidence during market downturns or life disruptions

- Fostering identity beyond work to prepare clients for retirement transitions

- Providing education tailored to specific circumstances rather than generic resources

“Money is emotional”, notes Liz Pfohl, Senior Business Development Manager at Sun Life Consulting. “The more an advisor understands a client’s mindset and emotional triggers, the better they can coach behaviour and build lasting trust.”

Most critically: the survey results suggest that financial confidence drives 64% more savings accumulation, making it 5x more powerful than financial literacy alone. The right advisor for you doesn’t just educate, they help build the confidence that can translate knowledge into action.

The full report includes strategies for each life transition and guidance for choosing an advisor who understands women’s realities.

About the research

Sun Life partnered with Ipsos to conduct online research with 653 Canadian women between December 27, 2024 and January 2, 2025. The sample comprised of:

- General population females (n=503)

- Affluent females aged 30-75 with investable assets of $100,000+ and personal income of $60,000+ (n=150) – oversampled to ensure adequate representation

Representative sample results are weighted to reflect the adult Canadian women population, with a credibility interval of ±3%.

Download the full report: Planning Through Change: How Women’s Life Transitions Reshape Financial Futures

This article is meant to provide general information only. Sun Life Assurance Company of Canada does not provide legal, accounting, taxation, or other professional advice. Please seek advice from a qualified professional, including a thorough examination of your specific legal, accounting and tax situation.