Client spotlight: West Fraser

Purchasing annuities for defined benefit plans since 2017

About West Fraser

West Fraser is a Vancouver-based forest products company that specializes in wood, pulp and paper and bioproducts. They employ over 6,000 Canadians across four provinces and 11,000 employees worldwide. They offer both defined benefit (DB) and defined contribution (DC) pension plans to their employees.

Elaine Jensen, General Manager, Human Resources (HR)

With 35 years at West Fraser, Elaine leads a variety of Canadian HR functions, including managing the company’s pension plans.

Earlier this year, Elaine shared details with us about West Fraser’s pension de-risking activities over the last decade. It included plan design, investment strategy and pension risk transfer (PRT). She further expanded on their successful repeat annuity transactions and why purchasing annuities is an important tool in reducing pension risk exposure.

“Pensions are a key part of our total compensation strategy.” – Elaine Jensen

The drivers

Providing pension benefits gives a competitive edge for recruiting and retaining employees, and it comes at a cost to the employer. West Fraser developed strategies to reduce pension risk and protect their employees financial future.

Their pension de-risking goals include:

- Contain costs and lock in plan funded status.

- Simplify plan administration and pension arrangements.

- Reduce risks within pension plans and protect pension plan payments for employees.

- Safeguard West Fraser’s core business and transfer risk off the balance sheet.

Since 2017, West Fraser has annuitized over $1B worth of pension liabilities through six transactions, protecting over 3,300 members.

“After much analysis and discussion with consultants, annuities were identified as the right solution for our well-funded plans.” Elaine also shares that, “Annuity purchases have been an excellent tool to help us reduce our pension risk exposure by close to a billion dollars within the last 5 years.”

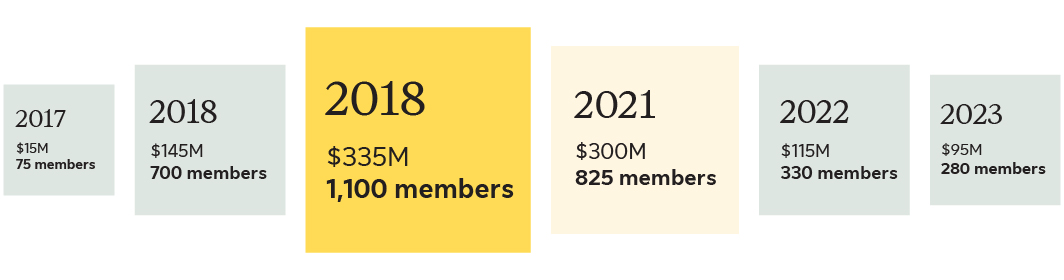

West Fraser’s pension de-risking journey

2017 – Their first transaction was an annuity buy-out for two small, closed plans. Two insurers split the transaction totaling $15 million. This was a learning experience for West Fraser that helped identify the steps needed to ensure successful transactions going forward.

2018 – West Fraser came to market with another annuity buy-out transaction. Two larger closed plans totaled $145 million, and the transaction was split between two insurers.

Building on this success, West Fraser came back to market later that year for two open plans. These Canadian salaried and hourly plans were West Fraser’s largest plans valued at $335 million. This annuity transaction transferred risk to two insurers, substantially reducing the number of retirees West Fraser was responsible for paying.

2021 – West Fraser confidently returned to market with a complex deal including seven open and closed plans. One of these plans was even a joint venture with a partner. Three insurers split the $300 million transaction.

2022 – Rising interest rates closed the pension funding gap and market conditions allowed for more affordable pricing. West Fraser de-risked an hourly open plan with inflation-linked liabilities worth $115 million with one insurer.

2023 – West Fraser came to market once again to purchase a $95 million annuity buy-out with one insurer. This transaction protects pension benefits for recent retirees of plans they previously de-risked with group annuity purchases.

West Fraser annuity purchases

Source: Sun Life estimates.

“There is no magic, there is no special sauce. We hope that others find something in our journey that they will find useful in theirs.” – Elaine Jensen

Keys to success

West Fraser is now a seasoned repeat buyer in the Canadian group annuity market. Here are some tips and learnings from their de-risking experience to date:

- Secure the right price - and the right partners.

- Collaborate with annuity purchase experts who can engage with insurers early in the process.

- Ensuring the combination of good plan’s funded position and annuity market conditions results in an ideal price situation.

- Consider other factors when selecting the right partners, like the insurers’ experience in the market, data protection and servicing.

- Prepare, understand your objectives and create a plan.

- Work with your consultants or actuarial professionals to get an estimate of the plan’s funded position.

- Prepare clean member data before going to market to get an accurate price quote.

- Get group annuity purchase experts to create a pricing estimate based on the annuity market ahead of quote day.

- Get approval from internal stakeholders ahead of quote day so there are no surprises.

- Build on your relationships with insurers.

- The transaction process requires being nimble and decisive while partnering with the right people.

- Gain familiarity with insurers before quote day to help identify the best partners for your company.

- Think about member experience.

- Tell members about the transaction.

- This can help educate them on the added protection for their pension benefits and remove any confusion around group annuity transactions.

West Fraser transacted to free up time for their core business. Their repeat transactions speak to the benefits of including group annuities in a pension risk mitigation strategy.

“We are thinking about how we can add value for plan sponsors. Whether that is bettering our pricing or creating innovative solutions.” – Dhvani Desai, Director Client Relationships, DB Solutions

A bright future

With experience de-risking several different plans, West Fraser recognizes there are more similarities between transactions than there are differences. Transacting as recently as fall of 2023, Elaine and her team continue to look for opportunities to de-risk West Fraser’s DB plans. They will move forward with the next transaction when it makes sense for their business.