Pension liabilities are determined using interest rates. Fluctuating interest rates can affect both the level of required cash contributions for the plan and pension costs disclosed in financial statements.

Is your company running a defined benefit pension division?

One way of looking at pension risk is to think about your defined benefit (DB) pension plan as a division in your company. It provides a product (an annuity) to a group of customers (your pension plan members). The business strategy of many DB pension divisions is to take risk in equity and bond markets. The hope is to earn excess returns and reduce the cost of providing pensions. There are innovative, affordable de‑risking solutions that can help you manage these risks in your pension plan.

Why is it hard to execute on this business strategy?

The business strategy involves taking risks, which can offset each other. For example, a successful bet on equities could be offset by an unsuccessful bet on interest rates. For the strategy to be successful, the pension plan needs to consistently place successful bets.

If your business strategy is succeeding:

- Your DB pension division is profitable

- Your cost of providing pensions decreases

If your business strategy is failing:

- Your DB pension division could lose money

- Your cost of providing pensions could increase

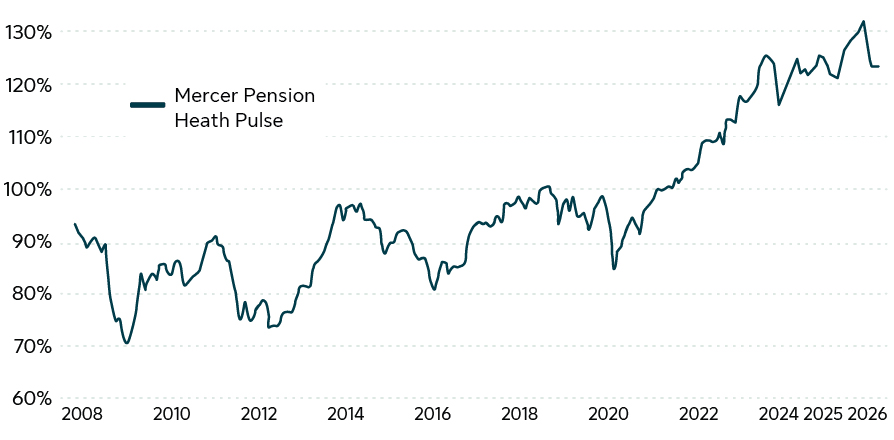

Source: Mercer Pension Health Pulse published April 2, 2026.

Over the past 18 years, how well have most Canadian pension plans performed?

The Mercer Pension Health Pulse shows funding levels of most pension plans took a wild roller coaster ride over the past 18 years. Since 2008:

- The average pension plan went above 100% solvency only two times.

- Most of the time, it stayed well below 100% with the lowest hitting close to 70% during the financial crisis.

- Solvency ratios for Canadian DB pension plans have continued to improve over the last 5 years, averaging well above 100%. Record-high funded statuses were reached in 2024, signalling the strongest position in nearly two decades.

- This continued strength gives plan sponsors the opportunity to reasses their pension risk strategy, taking risk off the table affordably.

A closer look at pension risks

The discount rates used to calculate liabilities reflect a large proportion of credit such as corporate bonds. If the pension plan does not have enough credit exposure, its assets may not move the same way as its liabilities.

Canadians are living longer than ever. It is great news for society, but for pension plans it means higher costs. When longevity improves so that an age 65 retiree is now expected to live one more year on average, this results in a 3-4% increase in cost for the pension plan (Sun Life). Pension payments need to be paid over a longer period. Investments in medical and anti-aging research and innovation could have a significant impact on longevity. (Source: Center for Disease Control, 2013)

Some pensions are increased periodically and linked to inflation. A change in inflation could lead to a change in pension funded status and required contributions if assets are not also linked to inflation.

Pension plans that invest in equities are exposed to additional risk because pension liabilities don’t behave like equities. Plans with significant equity exposure can experience more volatility in funded status and contribution requirements.

The yield on the pension plan assets should be at least equal to the liability discount rate. If there is a shortfall, the plan’s funded status could decrease as assets are not keeping up with liabilities.

This risk occurs when assets and liabilities aren't in the same currency. A change in foreign exchange rates could affect each of them differently. This could lead to a change in funded status and required contributions.

Get the latest insights on managing risk in your DB pension plan

Stay informed

Get the DB Solutions Insights email for the latest insights on managing DB pension risk.

Speak with an expert

We partner with plan sponsors to provide innovative, customized solutions that reduce DB plan risk.

Recent insights