Canadian Pension Risk Transfer Mid-Year Market Update

The case for action in Canada's pension risk transfer (PRT) market

The first half of 2026 has delivered a clear message to Canadian defined benefit (DB) plan sponsors: market conditions are favourable and the window for strategic action is open.

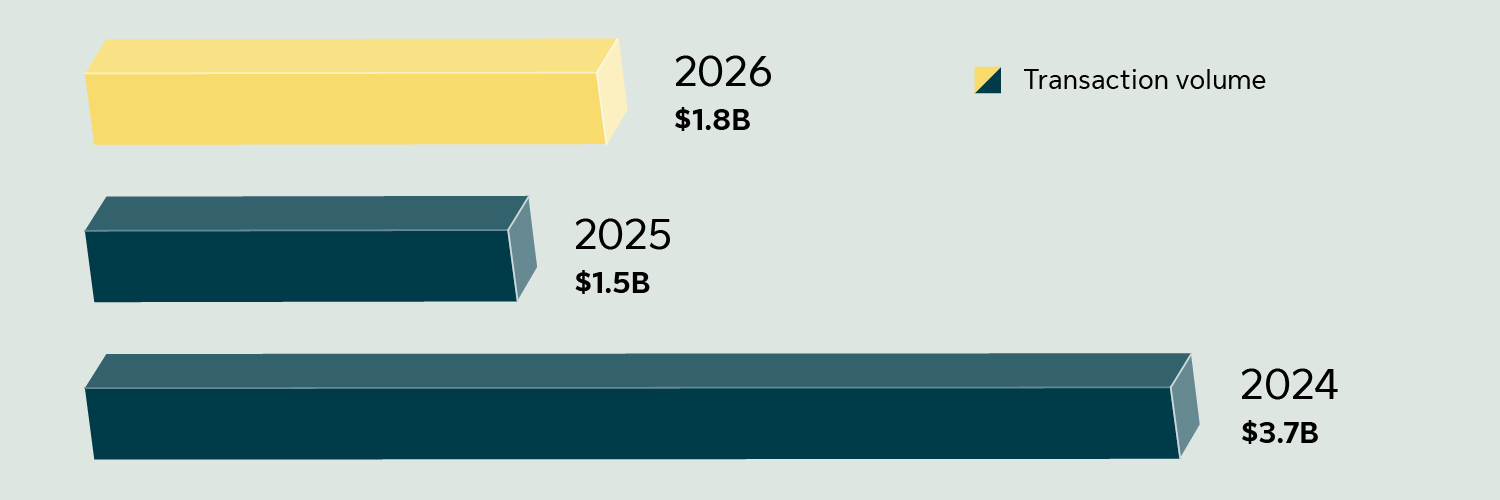

PRT market volume at June 30 ($B)

Sun Life estimates: 2026

Limra: 2024 & 2025

Based on the current transaction pipeline, we expect total PRT market volume for 2026 to be broadly in line with 2025. That said, the market remains well below the record-setting $11 billion reached in 2024, showing it can support much higher volumes than currently forecasted. This more measured pace is working in plan sponsors’ favour, creating attractive conditions for those looking to transact in 2026.

Benefits of transacting in a slower market

When PRT activity slows compared to peak years, many insurers become highly motivated to transact. This shift in dynamics typically translates to more competitive pricing and greater time and attention from insurers to structure customized solutions. For plan sponsors willing to act, this is a distinct advantage, particularly for larger, more complex transactions.

For more information on large and jumbo transactions, read this article:

Is 2026 the right time to de-risk your jumbo DB pension plan?

Pricing advantage: harvesting gains is within reach

Throughout 2025 and into the first half of 2026, annuity pricing has remained favourable. Annuity yields continue to exceed duration-equivalent corporate bond portfolios, even before accounting for risks transferred and expenses. Sun Life estimates a 4% improvement in annuity prices relative to corporate bonds since January 2020.1 This means plan sponsors can complete group annuity transactions while locking in accounting or funding gains, a particularly attractive outcome that combines risk transfer with financial benefits.

Each DB plan values their liabilities differently. You can explore if an opportunity exists by comparing the yield on an annuity – currently 4.9%2 – to your discount rate or expected return on assets. You can work with your consultant to get sample pricing from insurers and determine what pricing advantage may be possible.

Using surplus for strategic de-risking

Many DB plans continue to enjoy well-funded positions. For these plans, surplus can be more than a static asset – it’s an opportunity to act and secure positive outcomes for your plan and plan members. By pursuing a thoughtfully designed de-risking transaction, plan sponsors can:

- Access "trapped" surplus and improve cash flow

- Potentially reduce overall liabilities while completing a transaction

- Gain clarity on pension surplus that may exceed expectations

- Secure plan member benefits without unnecessary delay

Even highly complex DB plans can benefit from these opportunities. Innovative solutions now exist for unique plan challenges, like deferred premium payments, customized payment schedules aligned to illiquid assets and inclusion of both active and deferred members.

For more information on surplus and annuities, read this article:

A dynamic duo: DB pension surplus and group annuities

The bottom line: don't wait

Strategic de-risking delivers real results: reduced volatility, secured member benefits, and strong financial outcomes. With the market moving at a slower pace, insurers have significant appetite and capacity to transact, making it timely for DB plan sponsors to consider de-risking. As market conditions shift, so too will opportunities. The favourable environment of today won't last long.

The time to explore your options is now. Reach out to connect with your consultant or Sun Life's DB Solutions team and discover how your plan can benefit from current market conditions: DB.Solutions@sunlife.com

1 Based on the Canadian Institute of Actuaries annuity proxy.

2 Using the March 31, 2026, medium duration annuity proxy spread, published by the CIA, and CANSIM V39062 yields at March 31, 2026.