A dynamic duo: DB pension surplus and group annuities

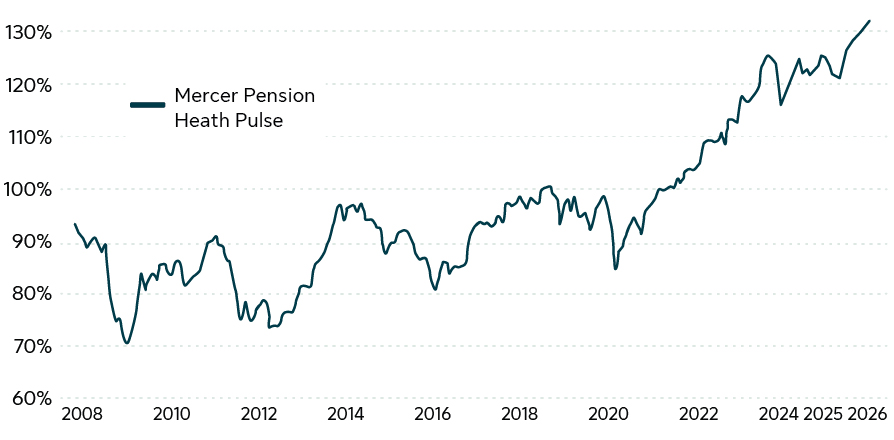

The defined benefit (DB) pension industry has been keeping us on our toes. Since 2022, momentum has shifted upward: after nearly twenty years of deficits, most plans now enjoy a welcome surplus. The Q4 Mercer Pension Health Pulse highlights this major shift – 92% of Canadian DB pension plans are now in a surplus position. What a climb!

The Mercer Pension Health Pulse

Source: Mercer Pension Health Pulse published January 5, 2026.

What does this mean for DB plan sponsors?

You can seize the opportunity to protect the gains in your DB pension plan. One way to do this is through a group annuity purchase, where pension risks are transferred to an insurer. These transactions can help you find a balance between the surplus strategies and risk management objectives in place to optimize your plan. There are many considerations that come into play when managing risks and protecting a plan’s funded position through a group annuity purchase, and we explore a few key ones here.

Future surplus generation

Looking ahead, if your plan sells passive bonds or partially divests its liability-driven investment (LDI) portfolio to fund a group annuity purchase, you’re effectively locking in gains for those assets. There’s still plenty of room to generate additional return with other asset classes too.

Passive bonds were likely not the main driver of surplus generation in the first place. Meanwhile, LDI portfolios remain essential for stability and can deliver incremental returns. The certainty of a group annuity can create a powerful combination: the group annuity can keep your plan out of deficit in the future for the covered population, while remaining assets can be positioned for surplus growth. A thoughtful mix of return-seeking investments, LDI and group annuities can protect gains while unlocking new opportunities.

Creating surplus

A group annuity transaction may create additional surplus. According to a recent white paper by Moody’s, when you factor in funding margins and Provision for Adverse Deviation (PfADs), an annuity purchase can positively impact the residual liabilities. The math can get technical on this topic, so working with your consultant is key.

- After a buy-out, you’ll likely see a net reduction in liability for remaining members, thanks to a higher discount rate from a larger allocation to return-seeking assets, which means stronger expected returns. Of course, a higher PfAD partially offsets this gain, but overall, you create more surplus, which you can use in different ways.

- For a buy-in, which is considered an investment of the plan, you’ll see a net reduction in liability if the annuity purchase yield is higher than the yield of the bonds being replaced in the overall portfolio. In addition, you’ll see a lower PfAD as the buy-in is exempt from the PfAD.

The current pension risk transfer (PRT) market is highly competitive amongst insurers and pricing for group annuities is attractive. Annuity yields have improved significantly in recent years. Sun Life estimates a 5% improvement in annuity prices relative to corporate bonds since January 2020.1

Comparing the yield on annuities to the yield of passive bonds

- Yield on annuity2 = 4.74%

- Yield on bond portfolio3 = 4.45% - 1.00% (risk/expense adjustment4) = 3.45%

Along with transferring investment and longevity risk to insurers, plan sponsors may consider a group annuity purchase to be a solid investment option – one that can lock in surplus or, considering the yields above, generate even more.

1 Based on the Canadian Institute of Actuaries annuity proxy.

2 Using the September 30th, 2025 medium duration annuity proxy spread, published by the CIA, and CANSIM V39062 yields at September 29th, 2025.

3 Based on a blend of the FTSE Canada All Corporate Bond Index and the FTSE Canada Long Term Corporate Bond Index at September 29, 2025 to achieve the same duration as the membership group used to determine the CIA medium duration proxy.

4Sun Life estimates as of September 30, 2025.

Liquidity management

Many mature plans now face liquidity challenges, and it’s common to be “cash flow negative” – meaning the plan is paying out more in benefits than it’s receiving in new contributions and investment income. For the cohort of members covered by a group annuity, that headache disappears: after the transaction premium is paid, you no longer have to manage liquidity for those individuals. Solving the liquidity challenge by paying the one-time transaction premium could prove easier than dealing with long-term liquidity headwinds.

Bottom line

The DB pension world is enjoying a rare surplus moment. There are smart ways to take advantage of your plan’s strong funded position that can benefit your plan and your plan members. Group annuities can be a powerful option that gives plan sponsors and members real peace of mind.